Opening a medical practice involves significant costs beyond medical knowledge. Sufficient initial capital is also vital for sustainability. Understanding these financial aspects is key to planning and securing funding for your practice. Read on to explore the main costs of starting a medical practice.

At Perform Practice Solutions we can help guide you in dozens of ways. We have seen all your challenges before!

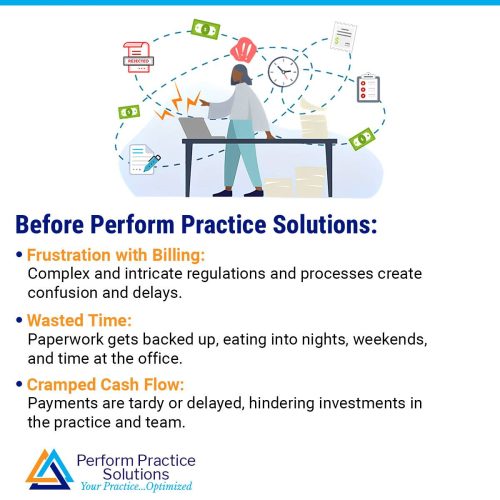

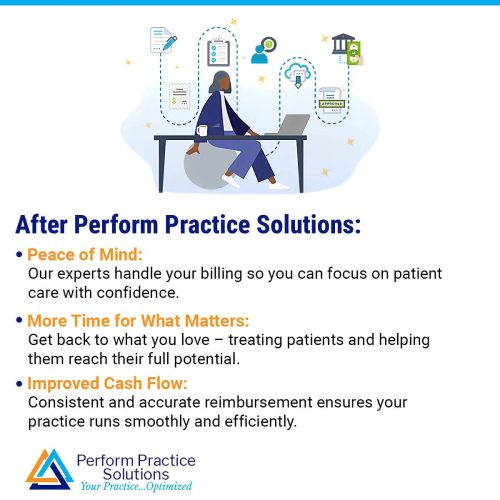

Perform Healthcare Billing Solutions is just one example of ways we can save you money — and your precious time. We created Perform Healthcare Billing Solutions because we saw so many of our practice clients getting burned by either their in-house biller or worse: their medical billing agency. You work so hard treating patients and running your practice, count on us to get you paid and fast. Our team of expert healthcare billing experts works around the clock to maximize your claims, get solid info from your front desk, and bill daily! We average a 3-week bill to paid time! Let us show you just how fast you can get paid — and how we can save you your hard-earned money. This is just one of our many supportive services. Book with us and let’s talk!

Starting a medical practice from scratch can be exciting, but to invest in a practice that has healthy cash flow and can scale and grow, you need to identify and plan for your medical practice start-up costs – so you can avoid as many surprises as possible.

There are many costs to consider when starting your own medical practice, and it might seem overwhelming at first, trying to plan for every contingency. Even if you know what costs you will be facing, it can be difficult to know how much all the costs will really be once you start implementing your business plan.

Medical Director’s new guide, ‘Calculating the cost of starting your medical practice’ offers a range of practical tips to help give you a clearer picture of what common costs you need to factor into your financial plan when starting out.

Through conversations with leading healthcare and financial experts, the guide offers tested and instantly practical advice about how to:

- Budget for expenses when starting out

- Cut costs with cloud software

- Calculate your set-up costs

- Manage your finances

- Finance your new practice.

Common medical practice start-up costs

You’ll get the full picture in the guide, but here’s a snapshot of some of the costs you need to consider if you’re thinking about starting a medical practice:

- Business plan development

- Preliminary accounting and legal advice to help you set up your new business entity

- Insurances and licenses, including medical malpractice insurance, workers compensation insurance and property insurance.

- Tenancy/lease bond agreements and property advice

- Design and fitout

- Telephone/internet installation

- Statutory requirements and legal advice

- Power connection

- IT infrastructure plan

- EFTPOS infrastructure

- Medical equipment/materials/machinery, office space, basic office equipment, fixtures and fittings

- Medical supplies and consumables

- Software, including practice management system

- Staff recruitment costs, training costs and wages

- Market research, marketing material, signage, and a marketing plan.

Medical Director CEO Matthew Bardsley explains the importance of a sound financial plan for any successful medical practice. “A future-thinking, smart financial plan for any medical practice needs to start with the premise that every dollar spent in healthcare needs to contribute to the most efficient and effective way of providing ideal levels of patient care,” says Bardsley.

“Investing in the smartest, most innovative clinical practice management methods from the start will help empower your practice to scale and achieve a competitive advantage, while adapting to the needs of your patients now, and in the future.”

Factor in one-time expenses versus ongoing costs

As you develop your financial plan, be sure to identify which costs will be one-off, and which will recur monthly, quarterly and annually. This forecasting will help you manage and set up your budget realistically, and better organize your cash flow from the outset. It’s important to operate this way from the very beginning, so you don’t get caught out in the future.

No one-size-fits-all financial plan

Your exact start-up costs will depend on the type of medical practice you are starting, and the region in which you are operating. Costs in the different categories can also vary across industries and regions. For example, a specialist practice may need to invest in specialist clinical management software, while a larger general practice would need to invest in a larger IT package tailored to a bigger team of medical professionals and support staff.

Setting realistic expectations

It’s better to err on the side of caution, overestimating both the time and money it takes to start a medical practice. Some experts recommend adding at least 10% on top of your total costs to cover any miscellaneous expenses or unforeseen fees and charges.

Meanwhile, how long it takes for your private practice to open its doors to generate revenue can make a huge impact on your cash flow and costs. Don’t set unrealistic expectations and never rush. If you get the timing wrong, costs, fees, charges and even penalties can escalate quickly – and you can find yourself under pressure to comply without enough of an income stream. This could have a significant impact on not only your practice as a business, but your professional reputation in the industry.

Where to begin?

Do as much research as possible to get a clearer picture of your budget requirements and set expectations of your costs versus cash flow when starting out. There’s plenty of great advice at your fingertips.

- Industry associations, like the RACGP, offer valuable advice for practitioners ready to start their own medical practices.

- Industry solution providers, like Medical Director, can offer support and advice on IT infrastructure costs for software that will scale and grow with your medical practice.

- Government bodies often offer tax and other incentives to help you when you set up your own business.

- Financial institutions can offer tailored financial advice and guidance as to how best to structure any loans.

- Tax and legal advisors can help you make sure you’re complying with all relevant legislation.

- Our free guide can step you through all the calculations involved in starting a medical practice.

A final word from Bardsley. “Investing in the right efficient and scalable tools and systems when setting up your practice, will help pave the way for you to grow your reputation as a leader in your industry, while balancing your work and lifestyle in a way that suits you and your family best. I wish you the best of luck in setting up your new medical practice, and helping more Australians find better patient-centric care.”

Dreaming of focusing solely on patient care in your practice? Our expert consultants can help you implement strategies to improve efficiency, patient satisfaction, and revenue. Let us handle your medical and dental billing. Schedule your free consultation with Kevin Rausch to get all your questions answered. Book here today. Follow us on IG.